Proactive fundraising sparks speculation over new business direction, M&A plans, and revenue concentration risks

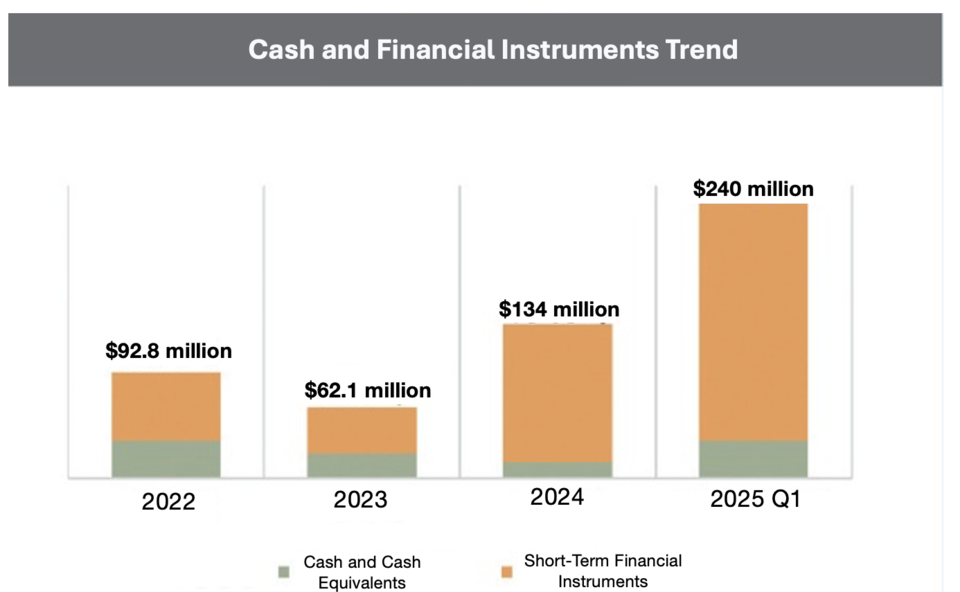

Leading biotech firm Alteogen is rapidly expanding its cash reserves. As of Q1 2025, the company holds approximately $240 million in cash and short-term financial instruments—an 80% increase year-over-year. This includes $113 million raised through a rights offering in February.

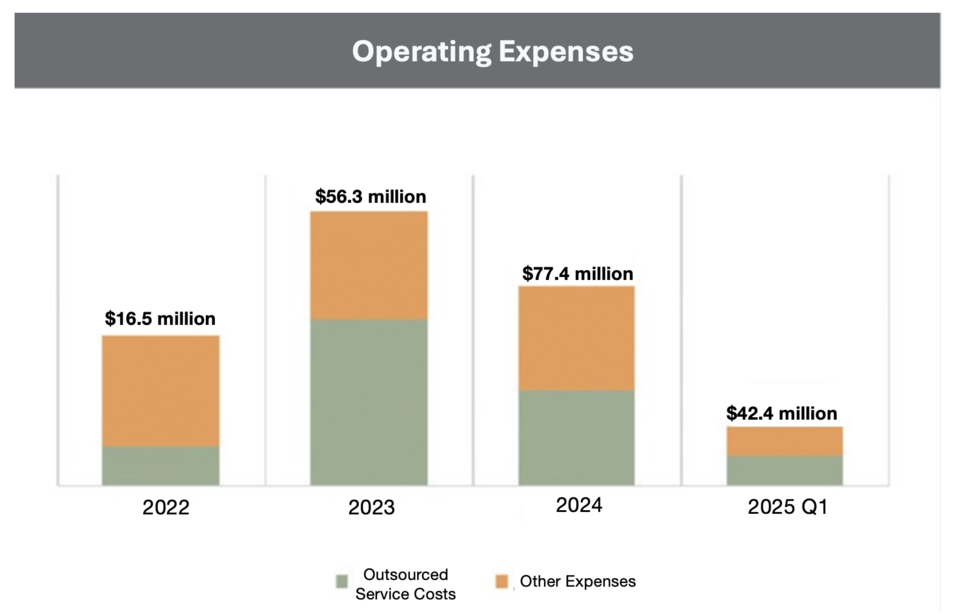

With stable or declining annual operating costs, the company’s aggressive capital accumulation is drawing attention from the industry.

Reported Cash Decline Contradicted by Rising Liquidity

While Alteogen’s financial statements show a decline in “cash and cash equivalents” since 2023, this metric excludes assets that mature beyond three months. When factoring in short-term financial instruments, the company’s actual liquidity has been on the rise. This indicates a healthier cash position than surface-level accounting data suggests.

In February 2025, Alteogen secured $113 million through a third-party allocation rights offering, issuing redeemable convertible preferred shares (RCPS). These investor-friendly shares offer redemption, conversion, and repricing rights, and are treated as liabilities under K-IFRS. Consequently, the raised capital increased the company’s debt ratio, despite its stated use: $73 million for working capital and $40 million for facility investments.

Operating and R&D Costs on the Decline

A review of Alteogen’s financials reveals decreasing operating and R&D expenses. In 2023, outsourced services made up 60.7% of operating costs, falling to 47.6% in 2024 and 50.8% in Q1 2025. The company attributes this to reduced contract manufacturing (CMO) fees as production becomes more efficient.

Based on Q1 data, projected 2025 operating expenses are estimated at $58.2 to $65.5 million.

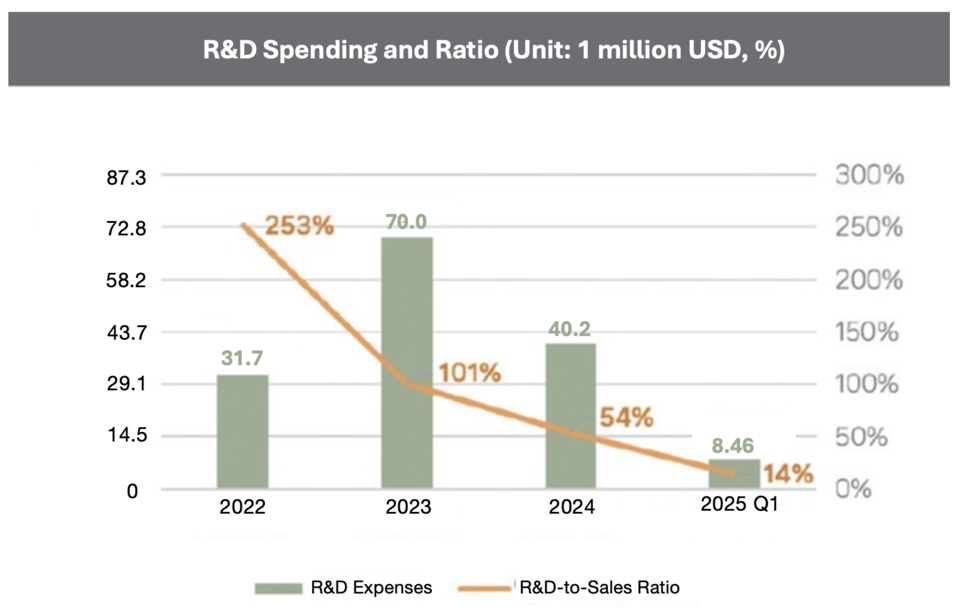

R&D expenditures have also declined. In 2024, Alteogen spent $40.2 million on R&D, compared to $8.44 million in Q1 2025—a figure that signals further reduction if annualized. While part of the decline may be attributed to growing revenue, the absolute decrease reflects a shift in spending patterns. Key R&D areas include ALT-B4-based programs, formulation optimization, and clinical development of biobetter candidates.

Despite these reductions, Alteogen is not in immediate financial distress—indicating the capital raise was a forward-looking move.

Possibility #1

ALT-B4 Revenue Dependency: Strategic Hedge or Risk?

One prevailing interpretation is that Alteogen secured liquidity in advance to hedge against uncertainties surrounding milestone revenues from its ALT-B4 out-licensing agreements.

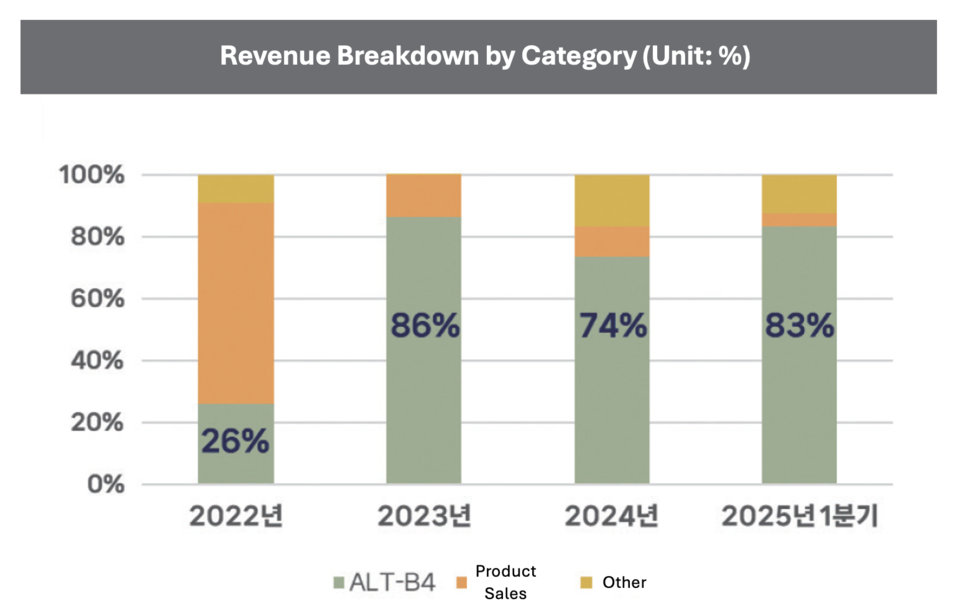

One interpretation of Alteogen’s preemptive funding is risk mitigation surrounding its ALT-B4 platform. While global licensing deals have fueled growth, the company’s revenue is highly concentrated in this single asset.

ALT-B4 accounted for 86.3% of revenue in 2023, 73.6% in 2024, and 83.2% in Q1 2025—amounting to $50.9–$58.2 million annually. While six licensing deals have been signed with companies like MSD, Daiichi Sankyo, Sandoz, and MedImmune, most programs remain in the clinical stage, with no commercial launches yet.

This dependency raises questions about long-term sustainability, particularly if clinical milestones are delayed or missed.

Possibility #2

Positioning for Business Expansion and M&A

Another rationale behind the fundraising could be a strategic shift in Alteogen’s business model. Of the $113 million raised, $40 million was earmarked for facility investments—potentially signaling a move toward in-house manufacturing. Such a shift would reduce reliance on licensing and position the company for direct product development and commercialization.

In addition, industry watchers speculate the company may be preparing for M&A or new platform investments, diversifying its revenue base and technological capabilities.

In a statement to HITnews, Alteogen described the capital raise as a “strategic move” to support facility expansion, business transformation, and development of next-generation platforms.

“While most of our manufacturing is currently outsourced to CMOs, we plan to build in-house production capabilities. This funding prepares us for that transition,” the company stated. It also confirmed that additional funding will go toward constructing a new headquarters and expanding its R&D team.

“Our Hybrozyme (ALT-B4) platform has matured, and we’ll continue pursuing out-licensing and commercialization. At the same time, we are now exploring new platform technologies, which will require additional R&D investment.”

Though details of future platforms remain undisclosed, Alteogen emphasized it will share updates once development advances.

Finally, the company reaffirmed its conservative financial approach, highlighting the importance of maintaining strong liquidity to weather external uncertainties and market volatility.

① Third-Party Allotment (Capital Increase via Third-Party Allocation)

A method of issuing new shares directly to selected external investors instead of offering them to existing shareholders. This allows the company to attract strategic investors, but can dilute existing shareholders’ ownership.

② Redeemable Convertible Preferred Shares (RCPS)

A type of preferred share that includes both redemption rights and conversion rights into common stock.

③ Redemption Right

A right allowing investors to request the company to repurchase their shares for cash after a certain period. This feature, unique to preferred shares, serves as a safety net to reduce investor risk.

④ Conversion Right into Common Shares

The right to convert preferred shares into common shares. Once converted, investors can exercise voting rights and realize capital gains through share trading.

⑤ Refixing (Conversion Price Adjustment)

A clause that allows the conversion price of preferred shares into common shares to be lowered. For example, if the company later issues new shares at a lower price, existing investors can adjust their conversion price to match. While this benefits investors, it creates accounting liabilities for the company, as the instrument must be treated as debt.